Northstar Realty Europe is delivering an attractive shareholder return from a portfolio of prime assets in strong European markets.

- Net Asset Value rose 27% since 12/31/16 to $20.50/share at 3/31/18

- Property Operating Expense declined from 24% of revenue in 2016 to 20% of revenue in 1Q18

- Overhead Expense declined from 6.0% of Net Assets in 2016 to 2.9% of Net Assets in 1Q18

- Discount to NAV of 30% for NRE compared to an average of 1% for 7 German listed peers

- Management and Manager incentives are now well-aligned with shareholders

A discount of 20% to NAV would fairly reflect NRE’s above average expense level and would imply a target price of about $16/share. If NRE builds a longer record of adding value and profitably recycling capital then a higher valuation could be reasonable.

BACKGROUND

Northstar Realty Europe holds assets from 3 acquisitions:

- SEB Portfolio, a US$1.3 portfolio of 11 properties purchased by Northstar Realty Finance (NRF) from SEB Immoinvest, an open-ended fund that was in liquidation

- Trias Portfolio, a US$0.5Bn portfolio of 37 properties acquired by Northstar Realty Finance from Provinzial Nordwest.

- Trianon tower, a US$0.6Bn 47-storey landmark building in Frankfurt acquired by Northstar Realty Finance

Shares of NRE were distributed to shareholders of NRF in October 2015. The price fell to a large discount to book value which fairly reflected the burdens of high overhead and a nearly perpetual management contract with Northstar Asset Management (see No Real Excitement for Northstar Realty Europe). Colony Capital expressed interest in acquiring the NRE management contract from NSAM, but unfortunately ended up buying all of NRF and NSAM instead (see Background of the Mergers, page 110). It’s easy to overlook NRE amidst the ensuing mess, but it’s one Northstar unit that is doing well.

Additional background on NRE’s current portfolio is in its March Investor Presentation, 1Q18 Financial Supplement, and SEC Filings.

ATTRACTIVE MARKETS

NRE’s portfolio is concentrated in a few Northern European markets which are currently enjoying strong demand, low vacancy rates, rising rents, and below average growth in supply.

Asset yields or cap rates in these markets are quite low, but still provide an attractive spread over mortgage financing costs and attractive premiums over government bond yields.

Additional information about these markets is available from Cushman & Wakefield, CBRE, Colliers, and JLL.

RISING NET ASSET VALUE

NRE began reporting EPRA Net Asset Value in mid 2016. Since 12/31/16 NAV has risen from US$15.89/share to $20.50/share at 3/31/18. Approximately 13% out of the 27% increase can be attributed to currency appreciation with the remainder due to asset revaluation.

Repurchase of 1.05mm shares in 1Q18 at an average price of $12.70 was likely responsible for accretion of about $0.14/share. Repurchase of an additional 2.38mm shares at an average price of $13.81 likely generated additional accretion of about $0.30/share so far in 2Q18.

FALLING EXPENSES

NRE has made significant progress at reducing property level expenses and corporate overhead.

The company has described opportunities to reduce expenses through internalization of functions that were previously outsourced. The impressive reduction in compensation expense reflects the 2017 vesting of most of the old Northstar equity grants in conjunction with the “change in control” triggered by the Colony Northstar merger. New smaller grants were made in 2018 that will be amortized over the next three years (see page 26 of the NRE 1Q18 10-Q filing for additional explanation).

SECTOR COMPARISON

NRE is the only US-listed REIT concentrating on European assets, but 7 German-listed REITs provide useful performance benchmarks.

NRE’s 2016 and 2017 expense levels were crippling, but if 2018 expenses can stay below 3% then the burden of the overhead could be fairly balanced by a discount to NAV of about 20%. If NRE were able to build a record of delivering superior returns through active management and profitably recycling capital after a holding period of 3-7 years then it could justify a higher valuation. On the 4Q17 conference call management declined to comment on an analyst question about whether it was interested in selling its largest asset, the Trianon Tower. The building is 98% occupied with an average remaining lease term of 6.2 years. If a buyer offered a premium price for this landmark asset then it could give NRE an opportunity to recycle capital into new undervalued properties or its own undervalued shares.

Note that Dream Global is dual-listed in Toronto and Frankfurt. NRE may want to consider a Frankfurt listing in the long-term in order to access a broader pool of investors.

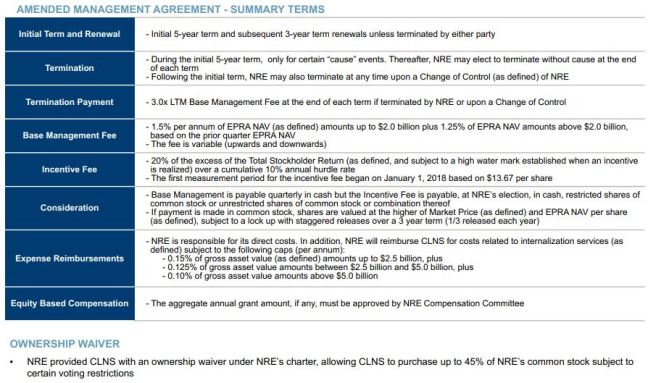

MANAGEMENT & MANAGER INCENTIVES

NRE signed a new management agreement with Colony Northstar effective 1/1/18. Key terms (from page 21 of the 4Q17 Supplement):

The incentive fee has a cumulative annual hurdle rate of a 10% shareholder return from a starting share price of $13.67. That means the threshold for the 2018 incentive is $14.54/share (assuming $0.60 additional return provided through dividends). And the incentive can be paid in shares valued at the higher of NAV or market. The new contract appears to provide strong alignment of interests between CLNS (the manager) and NRE’s public shareholders.

Incentive compensation of NRE executives is also now directly linked to shareholder return as disclosed in the Form 4 filings on 03/19/18:

NRE shares closed at $12.65 on the grant date of 03/15/18. They would need to reach about $19.23 (minus dividends) in order to deliver the Target Shareholder Return of 15%. The threshold for the 200% grant would be about $21.85 (minus dividends). If the stock hits those prices then I don’t think shareholders will be complaining about the extra management compensation. These targets show that management is heavily incentivized to get the share price up to Net Asset Value.

After the initial 5 year term the new management agreement can be terminated at a cost of 3X the base management fee, meaning an expense of 4.5% of NAV. If NRE were still trading at large discount (>20%) then it could be subject to activist pressure to liquidate. That would have been impossible under the old Northstar contract.

INVESTMENT CONSIDERATIONS

NRE can provide US investors with economic and currency diversification. If it continues to perform well then the company can deliver an attractive total return through a combination of rising NAV and narrowing discount to NAV. Cap rates in NRE”s core markets are low so NRE’s dividend yield is likely to remain modest and this may make it more difficult to attract attention from investors. The company’s high expense ratio can be balanced over time by a continuing discount to NAV and/or a track record of superior returns.

NRE’s manager, Colony Northstar, has cited Europe as a core market where it sees attractive long-term demand-supply fundamentals. In addition to the incentives within the management agreement, CLNS would benefit from raising the NRE’s share price to a level near NAV where it could grow through accretive acquisitions. A larger company would have a more diverse asset base, more efficient use of overhead, could justify a dual-listing.

DISCLOSURES & NOTES

The author is a shareholder of NRE and CLNS. The author does not make any recommendation regarding any investment in any company mentioned in this article. Investors are encouraged to check all of the key facts cited here from SEC filings and other external sources prior to making their own investment decisions.

One thought on “Northstar Realty Europe: Rising Asset Value and Falling Expenses”